The need to decarbonise the UK’s electricity supply as part of efforts to mitigate the effects of potentially catastrophic climate change is now little disputed. The UK has several targets to cut its domestic emissions to achieve an 80% reduction based on 1990 levels by 2050. This includes an interim target to source 30% of the UK’s electricity from renewable sources by 2020, as part of a wider 15% target for all forms of energy.

Much of the progress against these targets so far has been driven by government support schemes designed to make renewable technologies more attractive to investors (including businesses and households). As a result, 23% of electricity demand is being met by renewables.

Solar photovoltaic (PV) technology has played a significant role in this transition. Indeed, just over a year ago it was suggested that, with continued government support, solar PV might reach ‘grid parity’ by 2020. That would mean it could generate power at no greater cost to consumers than established (fossil fuel) technologies. Yet at this pivotal moment, and with little warning, support has been pulled away.

ROC-ing the boat

The solar PV industry, like other forms of renewable energy generation, has primarily received support from the Renewable Obligation (RO) scheme. PV has also been a recipient of the Feed-in Tariff (FiT), but this only covers projects of ≤5 MW, and is mainly used for smaller rooftop schemes on houses and commercial buildings.

The RO scheme started back in 2002, but it wasn’t until 2009 and the introduction of ‘banded’ support levels that investors began to look seriously at solar PV. Banding enabled higher levels of support for less established technologies. In 2011/12, solar PV could claim the highest possible level of support of two Renewable Obligation Certificates (ROCs) per MWh and the sector slowly began to gather momentum. Combined with a drop in the global costs of solar PV by 80% between 2008 and 2014, the commercial future for the industry looked bright.

The Government first announced its intention to terminate the RO back in July 2011, with a closure date of 31st March 2017. In May 2013, incremental annual reductions in support for solar PV were announced, through to the closure of the scheme. This gave a predictable timetable that developers could work with. It was therefore disappointing when last December DECC (now BEIS) announced it planned to close the RO to all solar PV projects as of April 2016.

Is the sun going down on the solar photovoltaic industry? Photograph by Alvesgaspar (CC BY-SA 3.0), via Wikimedia Commons.

The scale of the resulting slow-down in both the amount of new solar PV entering the planning system and the capacity becoming operational has not been widely appreciated. Several PV companies have shut up shop while others have scaled back operations, resulting in thousands of job losses. Activity in the sector has almost come to a standstill, with new planning applications drying up and just 22 MW becoming operational in the last 3 months.

Best laid plans

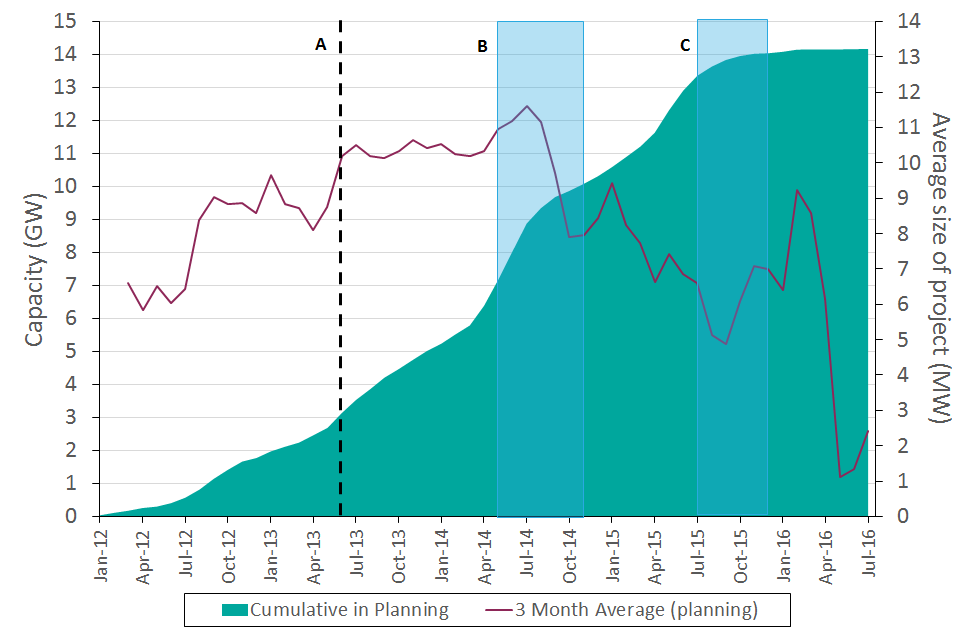

Eunomia’s work on the renewable energy planning database (REPD) for BEIS entails regularly examining changes within the solar PV industry. We have therefore been able to track the amount of solar PV entering the planning system. Based on the August 2016 Edition of the REPD, I’ve analysed the impact the unexpected RO change has had on the number of planning applications and related capacity of solar PV farms for which an application has been submitted. The graph below shows the total, cumulative solar PV capacity for which applications have been submitted nationwide, alongside a 3-month rolling average of the size of the facilities for which applications were made.

The cumulative total of solar PV in planning, since January 2012. Source: Eunomia/REPD

In early 2012 a slow but steady increase began in the capacity entering the planning system. In May 2013 (line A) the Government announced its timetable for closing the RO; the amount of capacity being applied for then accelerated from July 2013.

Subsequently, in May 2014, the Government published a consultation on closing the RO scheme to solar PV projects >5 MW (at the start of area B). The consultation concluded in November 2014, with a decision to go ahead with the change; to qualify for subsidy, projects of >5 MW already in the pipeline had to be operational by 31st March 2015.

This precipitated a surge in new planning applications, nearly 4 GW (4,000 MW) worth between May and October 2014. During the same period, the average size of projects peaked (at a little above 11 MW), as developers, anticipating a negative result from the consultation, rushed to make applications for projects >5 MW, even before it had concluded.

A second surge in applications came in the run up to July 2015, with almost 600 MW of capacity being applied for in a single month. Again, developers were perhaps anticipating discouraging news, this time from the consultation on closing the RO to solar PV projects ≤5MW, which was published on 22nd July 2015. From then, until the result of the consultation was published in December (area C), applications slowed. Since the Government resolved to close the RO scheme to solar PV, the cumulative total has levelled off, showing that in the absence of RO support, little solar PV has been applied for.

System failure

While over 14 GW of solar PV has entered the planning system since the start of 2012, not all of this has actually been constructed. In fact, analysis of operational capacity presented in the graph below shows that just under 50% of projects entering the planning system have successfully reached operational status.

The cumulative total of solar PV in planning shown against operational capacity, since January 2012. Source: Eunomia/REPD

An annual peak at the end of each RO banding period (which runs from the 1st April to the 31st March) is clearly visible, as projects had to be fully operational to claim within a given year. Projects missing the deadline were still eligible to claim in the following year, but would receive less support due to the annual banding reductions.

The largest number of projects became operational in March 2015, just before the RO closed to projects >5 MW: over 2.1 GW came online in that month alone (line A). The second highest point came a year later in March 2016, when over 1.1 GW was completed in a single month ahead of the RO closing to PV (line B). There remains a ‘grace period’ until March 2017 for projects which met certain criteria (for example, planning consent was in place) at the time the early withdrawal of RO support was announced. As a result, further projects are becoming operational, but at a small fraction of previous levels of activity.

Prior to March 2016, several large scale projects opted to reduce their total size as they could only claim the RO support for a maximum of 5 MW after the end of the 2014/15 financial year, despite already having planning permission for larger sites. This in part explains why the spike for the end of the RO is lower than for the preceding year. In the financial year 2014/15, a total of 3.1 GW of solar PV was built across 276 projects; of these, 204 were ≥5 MW. Compare this with the following year, where a total of 2.0 GW across 289 projects was built out: only 80 of these were ≥5 MW, while 209 projects were below 5 MW.

Out of the sun

The analysis shows a clear slow-down in the deployment of solar PV across the UK. The RO will result in some further grace period projects becoming operational prior to April 2017, but the level of the FiT is now insufficient to support investment. It remains to be seen whether solar PV will continue to be eligible for support under the Contracts for Difference (CfD) mechanism (three projects were awarded CfDs during the last auction). If it does, the funding available for established technologies like PV beyond 2016/17 is just £15m, compared to £50m in the previous year. Irrespective of eligibility, however, CfD strike prices (effectively caps) are far lower than the previous levels of support under the RO. The chances are therefore slim that projects with little time left on their planning permission will ever be built.

Greg Clark, secretary of state for the newly created Department of Business, Energy and Industrial Strategy (BEIS) has maintained the need to ‘upgrade’ all areas of the energy sector, including the “cleanness of our energy supplies.” For solar PV, it looks as though the government believes it has already played its part. The best prospect for solar PV developers now seems to be to develop ‘private wire’ schemes, within which power is sold directly to customers at mutually beneficial rates, but we are yet to see how successful this approach will be.

Leave A Comment