by Adam Baddeley and Chloe Bines

Under the EU Renewable Energy Directive (RED), the UK is legally committed to delivering 15% of its energy demand from renewable energy sources by 2020. Achieving this ambitious target will require a substantial decarbonisation of the energy system and the UK Renewable Energy Roadmap published by DECC set a target for 13GW of installed onshore wind turbines by 2020, 18GW of offshore wind and as much as 20GW of solar PV.

Alongside this planned transformation of our electricity generating infrastructure, electricity demand is also evolving. A low-carbon energy system will require greater electrification of heat and transport whilst smart grid technologies offer the potential to change demand patterns.

Together, these changes present an enormous challenge for the UK electricity grid, which currently relies on switching off and on conventional large-scale, centralised electricity generation to meet a reasonably established pattern of demand. Integration of more dispersed renewable energy generation into the market will require greater flexibility in both supply and demand in order to manage:

- unpredictability and variability of intermittent generation from renewable energy sources such as wind and solar; and

- changed patterns of demand, with the potential for higher demand peaks as more of our power needs are met by electricity.

If electricity could be stored effectively, it would provide a tremendous scope for flexibility. Electricity could be captured when the sun shines and the wind blows, and released when demand is at its greatest, reducing the need to build generating capacity to meet peak demand, and offering an alternative to conventional network reinforcement.

What the future has in store

Grid-scale electricity storage technologies are currently in limited use in the UK. Currently, the majority is provided by pumped hydroelectric storage, such as the Dinorwig Power Station. Whilst such technology is proven and can provide significant storage capacity, it is expensive, reliant on the right kind of valley landscape, and may entail the loss of habitats and the relocation of inhabitants.

Blast and dam: the development of the Dinorwig plant relied on local geology and historic quarrying to make it a viable example of large-scale energy storage. Photo by Dennis Egan, via Wikimedia Commons.

There are, however, a growing number of innovative storage technologies in the research and demonstration or early commercial stages, from flywheels to superconducting magnetic storage and advanced battery technology. These technologies have the potential to provide an array of functions to serve the electricity grid, from assuring power quality to deferring electricity grid infrastructure upgrades to integrating intermittent renewable generation.

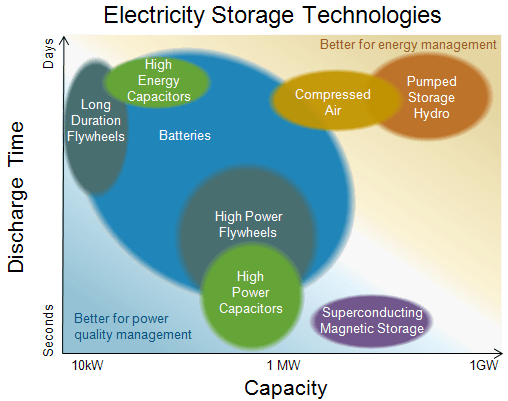

- Energy management across long timescales: Variations in daily, weekly, and seasonal electricity demand are relatively predictable. Higher-capacity technologies capable of outputting electricity for extended periods of time, such as pumped hydroelectric storage or compressed air energy storage, can moderate the extremes of demand over these longer periods. These technologies provide solutions for energy management, reducing the need (and associated costs) for generating capacity. For storage operators, the opportunity to buy power when prices are low and sell when prices are high gives rise to arbitrage opportunities from which they can profit.

- Power quality management across shorter timescales: Rapid demand fluctuations require rapid response technologies like flywheels, super-capacitors, or a variety of batteries, which will have a smaller capacity but which are more readily constructed and can be called into service quickly. By responding to short-timescale fluctuations, operators can keep the voltage and frequency characteristics of the grid’s electricity consistent within narrow bounds. This provides an expected level of power quality, an important attribute of grid electricity, as momentary spikes, surges, sags, or outages—can cause inconvenience or even harm electronic devices.

Store draw: each technology has a different balance of capabilities. Image courtesy of U.S. Energy Information Administration.

Balance of power The range of electricity storage technologies and their differing characteristics (i.e. discharge times, capacity, energy density) are suited to a range of applications. Consequently there are a number of potential business opportunities for electricity storage, which are illustrated below.

Store attraction: electricity storage has myriad potential benefits. Image by Adam Baddeley.

However, standing in the way of achieving these benefits are several obstacles, not least of which is cost. The price per kW (or kWh) varies considerably across technologies. Although costs appear to be coming down as the industry grows, the economics will remain challenging so long as more conventional alternatives, such as the cost of grid infrastructure reinforcement, remain cheaper.

The high development and capital costs demand significant returns to make storage technologies an attractive prospect to lenders and investors. This is unlikely to be attainable through a single market opportunity, and storage owners/operators will need to operate across markets and access multiple revenue streams in order to make money, which regulations and energy market requirements may make difficult. This creates some substantial complications in energy storage business models.

Money is power

This in itself might be less of a problem if lenders and investors had cast iron trust in the technology. However, while a number of storage technologies have a technical track record, their limited deployment in the UK means that they don’t have such confidence. This is a significant barrier to securing loan finance for a first wave of commercial projects, and electricity storage technologies will need to rely on more costly equity investment.

Whilst the range of potential applications suggests a wide market for electricity storage, the technology throws up a number of issues around ownership. Distributed Network Operators (DNOs) might be the obvious choice to own and operate storage, integrating it into the tower and cable infrastructure to assist with balancing supply and demand and to increase capacity for distributed generation.

However, electricity storage is technically classified as ‘generation’ and current market regulations preclude DNOs owning generating capacity greater than 10MW. This may be sufficient for many applications within the distribution network, but there is also limited flexibility for DNOs to sell power to the wholesale market. Since selling power is a key revenue stream for storage technology, this limitation makes storage an unattractive proposition for DNOs. Although they see electricity storage as playing a role within grid management, the preference seems to be for it to be owned and operated by third parties.

Other potential owners include distributed generators and energy intensive industries. However, at present these organisations lack expertise when it comes to integrating the technology with their operations and optimising charging and discharging to maximise returns.

The corridors of power

Although there has been little policy support for energy storage to date, increasingly DECC, Ofgem and National Grid are coming to regard storage, alongside demand side response (DSR), as a means of enabling optimisation of the electricity market and assist in achieving security of supply. This has resulted in the consideration and implementation of measures designed to establish broader and more flexible development of storage capacity as part of the current process of Electricity Market Reform (EMR) and revisions to the way the grid is balanced by National Grid.

Financial incentives specifically for electricity storage still appear a remote prospect, however. Instead, storage will need to compete in the capacity market being introduced through the EMR. However, the rules governing the capacity market present a challenging proposition for storage technologies due to the apparent requirement to be able to deliver power for an indefinite period following a ‘Capacity Market Warning’ and/or system stress event.

At this stage, the industry needs to think creatively. The early market winners are likely to be those who go beyond ‘selling plant’ and instead offer a range of services and solutions, including flexible generation, storage and grid reinforcement services. In order to stimulate interest among clients in the distributed generation and energy intensive industry sectors, innovative business models will be required.

These could include third party financing, ownership and operation of assets on the client’s behalf, potentially through an Energy Service Company (ESCO). Alternatively, there may be scope for storage pioneers to work on a revenue sharing basis with partners, whether this comes from electricity sales, balancing services or the capacity market. However, if energy storage is to become a substantial part of our power infrastructure, the capital costs of technologies will need to continue to decline. Only then will storage be able to compete with more conventional solutions such as additional generating capacity, grid management and reinforcement.

Despite the challenges, recent technological developments make this an exciting time for electricity storage. Storage technologies may not yet be established as proven, but progress is being buoyed by the growth in renewable generation and attendant concerns over continuity of supply. Storage appears to be a critical component in decarbonising our electricity, yet this is a technology still seeking a business model. The industry still needs to think creatively to identify who to work with and how so as to bring together the finance and the deployment opportunities to bring storage solutions into play.

My inventions include inexpensive energy storage for any surplus

electricity that could be converted to heat and regenerated in my CSP

Solar, just as energy of Sun that can also be stored. Therefore my PSs

would be able to work 24/365 and even give double quantity at “Peak

Consumption” periods. However Patenting process is not finalized so I canot

explain it publicly.

Regards from Croatia, the Homeland of Engineer Nikola Tesla!